Which Of The Following Accounts Does Get Closed? A. Service Revenue

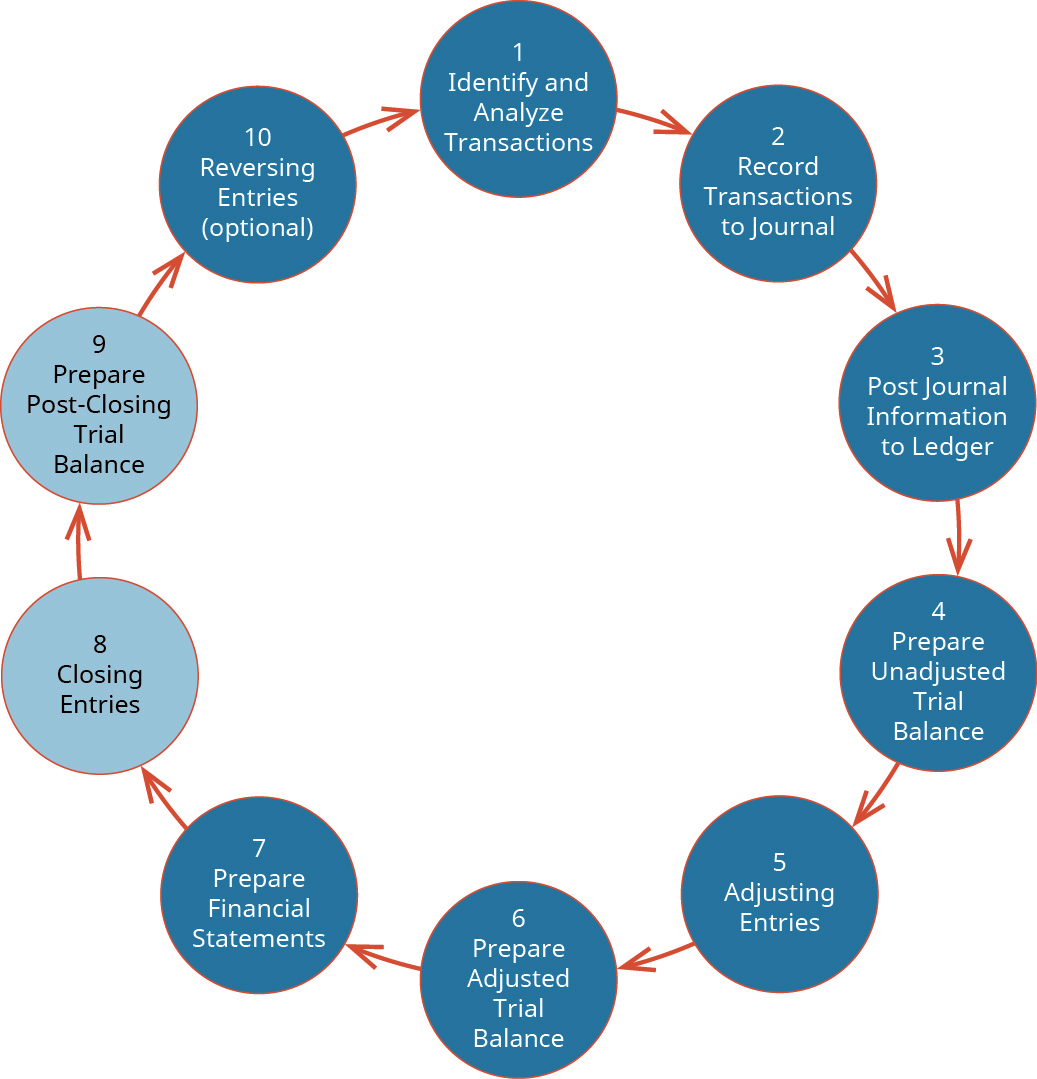

Completing the Accounting Bicycle

25 Describe and Prepare Endmost Entries for a Business

In this chapter, we complete the final steps (steps 8 and ix) of the accounting cycle, the closing procedure. You will notice that we exercise not embrace footstep 10, reversing entries. This is an optional pace in the accounting cycle that you will acquire about in future courses. Steps 1 through four were covered in Analyzing and Recording Transactions and Steps 5 through seven were covered in The Adjustment Process.

Our discussion here begins with journalizing and posting the closing entries ((Figure)). These posted entries will then translate into a post-closing trial balance, which is a trial balance that is prepared after all of the closing entries have been recorded.

Terminal steps in the accounting cycle. (attribution: Copyright Rice University, OpenStax, nether CC By-NC-SA 4.0 license)

Should You lot Compromise to Please Your Supervisor?

Yous are an accountant for a pocket-sized issue-planning business. The business has been operating for several years merely does not take the resource for accounting software. This means yous are preparing all steps in the accounting cycle by hand.

Information technology is the end of the calendar month, and you have completed the post-endmost trial balance. You find that there is still a service acquirement business relationship residue listed on this trial residuum. Why is information technology considered an error to take a revenue business relationship on the post-endmost trial balance? How practise you fix this error?

Introduction to the Endmost Entries

Companies are required to close their books at the stop of each fiscal year so that they tin can prepare their almanac financial statements and tax returns. Withal, most companies set monthly financial statements and close their books annually, so they have a clear picture of company performance during the year, and give users timely information to make decisions.

Closing entries prepare a company for the next accounting period by immigration any outstanding balances in certain accounts that should not transfer over to the adjacent period. Closing, or clearing the balances, means returning the account to a goose egg rest. Having a null balance in these accounts is important so a company can compare performance beyond periods, specially with income. It also helps the company keep thorough records of account balances affecting retained earnings. Revenue, expense, and dividend accounts bear upon retained earnings and are closed and so they can accumulate new balances in the side by side period, which is an application of the time period supposition.

To farther clarify this concept, balances are closed to clinch all revenues and expenses are recorded in the proper menstruum and and then start over the following period. The revenue and expense accounts should start at zippo each period, because we are measuring how much revenue is earned and expenses incurred during the menstruum. Withal, the cash balances, as well as the other balance canvas accounts, are carried over from the cease of a current flow to the beginning of the side by side period.

For example, a shop has an inventory business relationship balance of $100,000. If the shop closed at 11:59 p.m. on January 31, 2019, then the inventory residuum when it reopened at 12:01 a.m. on Feb 1, 2019, would however be $100,000. The residuum sail accounts, such equally inventory, would carry over into the side by side period, in this case February 2019.

The accounts that demand to start with a clean or $0 residue going into the next accounting period are revenue, income, and any dividends from Jan 2019. To determine the income (turn a profit or loss) from the month of January, the store needs to close the income statement data from January 2019. Zeroing January 2019 would then enable the store to calculate the income (turn a profit or loss) for the adjacent calendar month (February 2019), instead of merging it into January'due south income and thus providing invalid information solely for the month of February.

However, if the company likewise wanted to keep yr-to-engagement data from month to month, a split up gear up of records could be kept equally the visitor progresses through the remaining months in the year. For our purposes, assume that we are closing the books at the terminate of each calendar month unless otherwise noted.

Allow'due south look at some other example to illustrate the indicate. Assume you own a small landscaping business. Information technology is the end of the twelvemonth, Dec 31, 2018, and y'all are reviewing your financials for the entire year. Yous meet that you lot earned $120,000 this twelvemonth in acquirement and had expenses for rent, electricity, cable, internet, gas, and food that totaled $70,000.

You lot as well review the following information:

The adjacent day, Jan one, 2019, you get ready for piece of work, just before you go to the office, y'all make up one's mind to review your financials for 2019. What are your year-to-date earnings? So far, y'all have not worked at all in the current year. What are your total expenses for rent, electricity, cablevision and internet, gas, and food for the current year? You have also non incurred whatever expenses yet for rent, electricity, cable, internet, gas or food. This means that the current balance of these accounts is nothing, because they were airtight on Dec 31, 2018, to complete the annual accounting period.

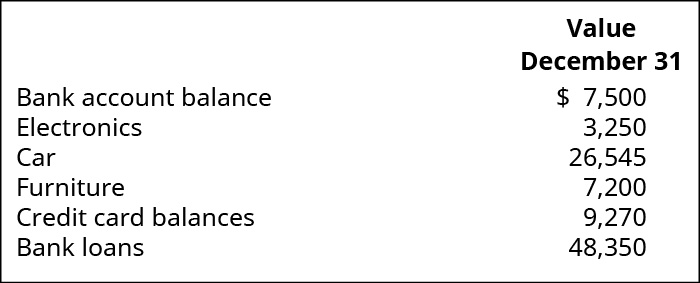

Next, you review your assets and liabilities. What is your electric current bank account balance? What is the electric current volume value of your electronics, car, and furniture? What most your credit card balances and banking company loans? Are the value of your avails and liabilities at present cipher considering of the beginning of a new year's day? Your car, electronics, and furniture did not suddenly lose all their value, and unfortunately, you lot still have outstanding debt. Therefore, these accounts all the same have a residual in the new year's day, because they are not closed, and the balances are carried forward from December 31 to January 1 to start the new annual accounting period.

This is no different from what will happen to a visitor at the stop of an accounting menstruum. A company volition run into its acquirement and expense accounts set back to zero, but its avails and liabilities will maintain a rest. Stockholders' equity accounts will likewise maintain their balances. In summary, the accountant resets the temporary accounts to null past transferring the balances to permanent accounts.

Understanding the accounting wheel and preparing trial balances is a practice valued internationally. The Philippines Center for Entrepreneurship and the government of the Philippines agree regular seminars going over this wheel with minor business organisation owners. They are too transparent with their internal trial balances in several key regime offices. Check out this article talking about the seminars on the accounting cycle and this public pre-closing trial residuum presented past the Philippines Department of Wellness.

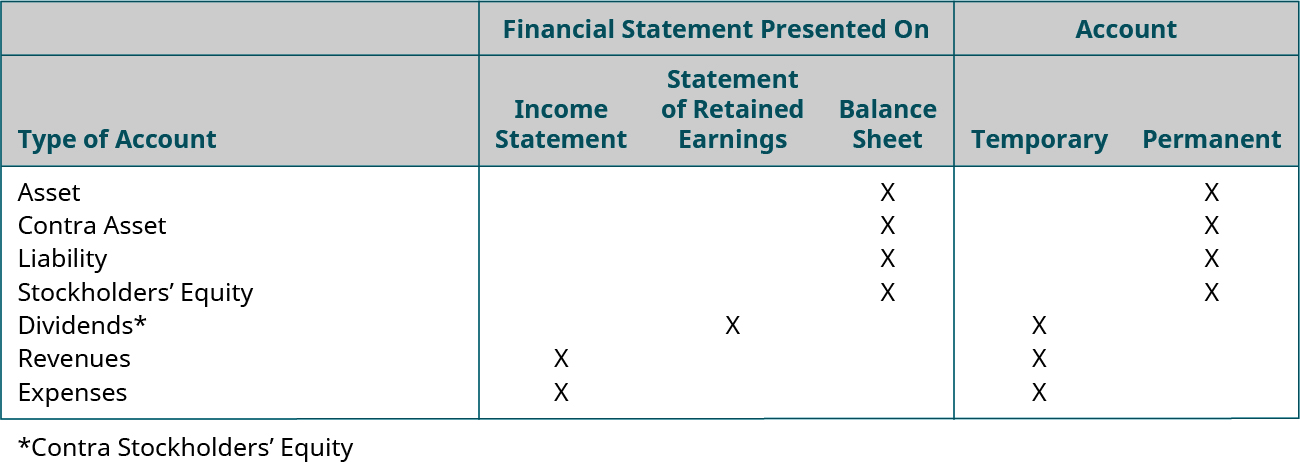

Temporary and Permanent Accounts

All accounts can exist classified as either permanent (real) or temporary (nominal) ((Figure)).

Permanent (real) accounts are accounts that transfer balances to the next period and include balance canvas accounts, such every bit assets, liabilities, and stockholders' equity. These accounts volition non be set back to nothing at the beginning of the side by side period; they volition keep their balances. Permanent accounts are not part of the closing procedure.

Temporary (nominal) accounts are accounts that are closed at the cease of each accounting catamenia, and include income statement, dividends, and income summary accounts. The new business relationship, Income Summary, will be discussed presently. These accounts are temporary because they go along their balances during the current accounting period and are ready back to zero when the period ends. Revenue and expense accounts are airtight to Income Summary, and Income Summary and Dividends are closed to the permanent account, Retained Earnings.

Location Chart for Financial Statement Accounts. (attribution: Copyright Rice University, OpenStax, under CC Past-NC-SA 4.0 license)

The income summary account is an intermediary between revenues and expenses, and the Retained Earnings business relationship. It stores all of the closing information for revenues and expenses, resulting in a "summary" of income or loss for the period. The balance in the Income Summary business relationship equals the cyberspace income or loss for the menstruum. This remainder is then transferred to the Retained Earnings business relationship.

Income summary is a nondefined account category. This ways that it is not an nugget, liability, stockholders' equity, revenue, or expense account. The business relationship has a cypher balance throughout the entire bookkeeping period until the closing entries are prepared. Therefore, it will not appear on any trial balances, including the adjusted trial balance, and will non appear on any of the financial statements.

You might be asking yourself, "is the Income Summary business relationship even necessary?" Could nosotros merely shut out revenues and expenses directly into retained earnings and not have this extra temporary account? We could practise this, but past having the Income Summary business relationship, you get a balance for net income a second time. This gives you the balance to compare to the income statement, and allows you lot to double check that all income statement accounts are closed and accept correct amounts. If you put the revenues and expenses directly into retained earnings, you will not see that check figure. No matter which manner you choose to close, the same last remainder is in retained earnings.

Permanent versus Temporary Accounts

Following is a list of accounts. State whether each account is a permanent or temporary business relationship.

- rent expense

- unearned revenue

- accumulated depreciation, vehicle

- common stock

- fees acquirement

- dividends

- prepaid insurance

- accounts payable

Solution

A, E, and F are temporary; B, C, D, G, and H are permanent.

Permit's at present wait at how to prepare closing entries.

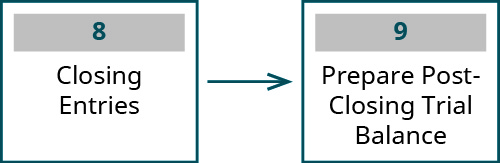

Journalizing and Posting Closing Entries

The eighth stride in the accounting cycle is preparing endmost entries, which includes journalizing and posting the entries to the ledger.

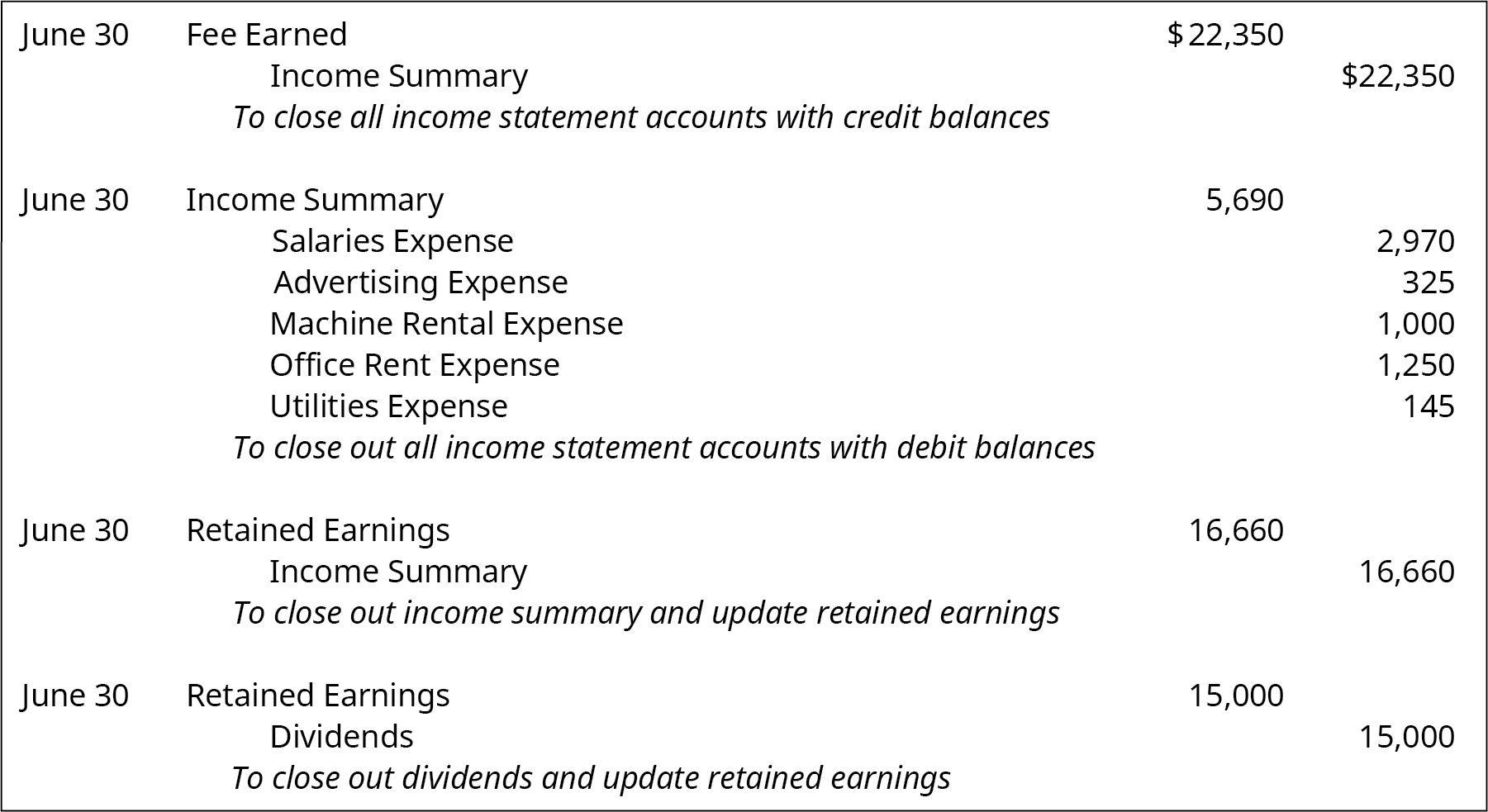

Four entries occur during the closing procedure. The get-go entry closes revenue accounts to the Income Summary account. The second entry closes expense accounts to the Income Summary business relationship. The third entry closes the Income Summary account to Retained Earnings. The 4th entry closes the Dividends account to Retained Earnings. The data needed to prepare closing entries comes from the adjusted trial residuum.

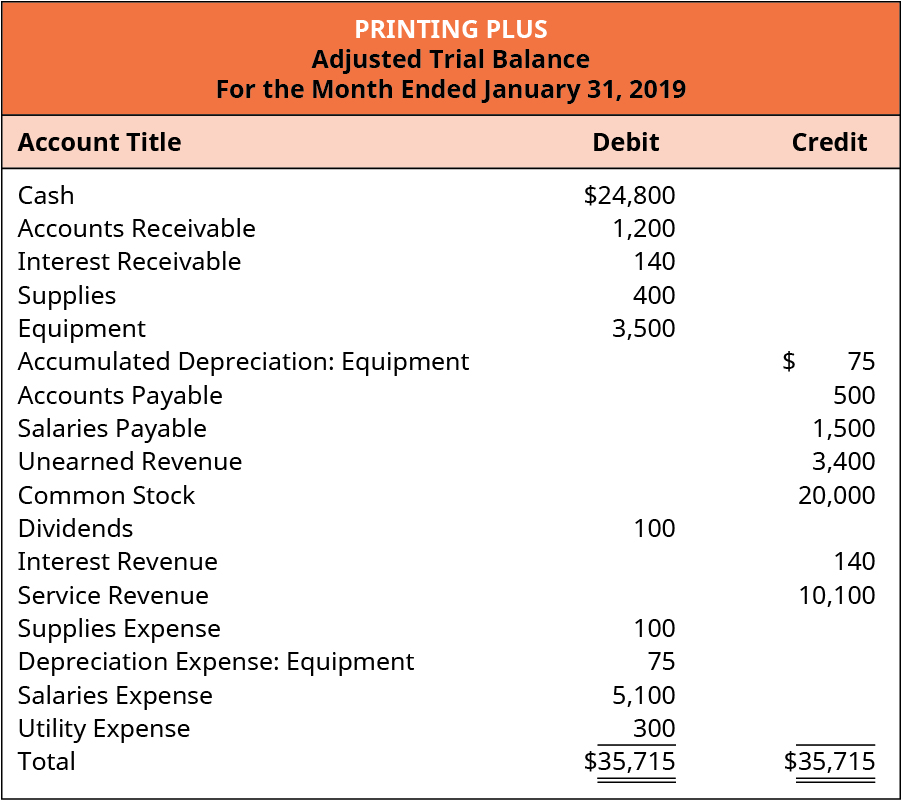

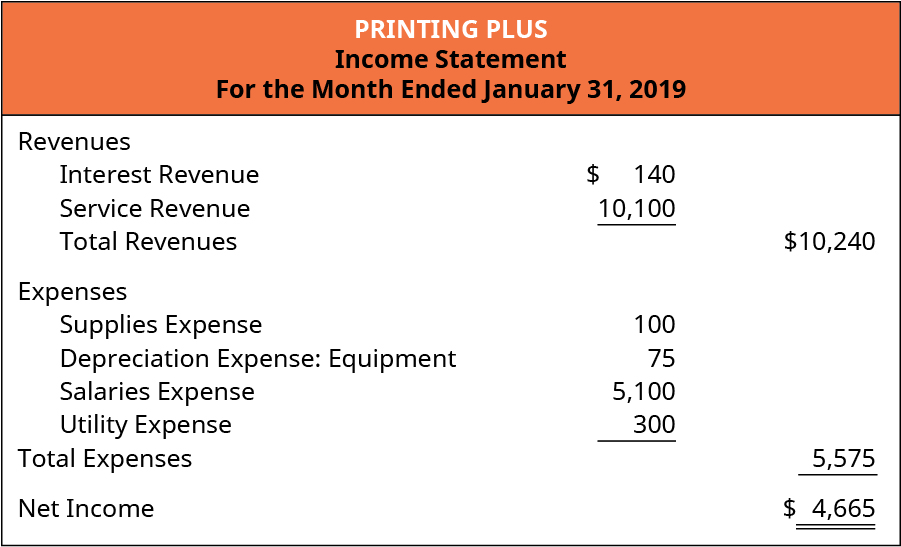

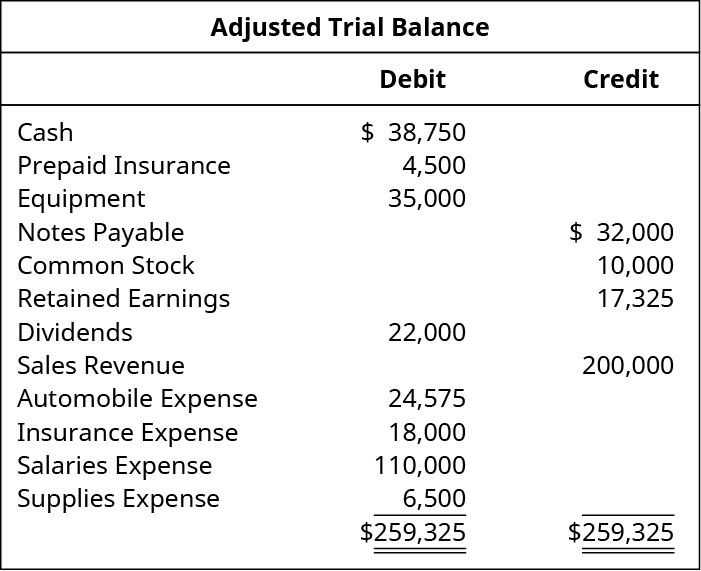

Let's explore each entry in more item using Printing Plus'due south data from Analyzing and Recording Transactions and The Adjustment Procedure as our case. The Printing Plus adjusted trial remainder for January 31, 2019, is presented in (Effigy).

Adjusted Trial Balance for Printing Plus. (attribution: Copyright Rice Academy, OpenStax, under CC BY-NC-SA iv.0 license)

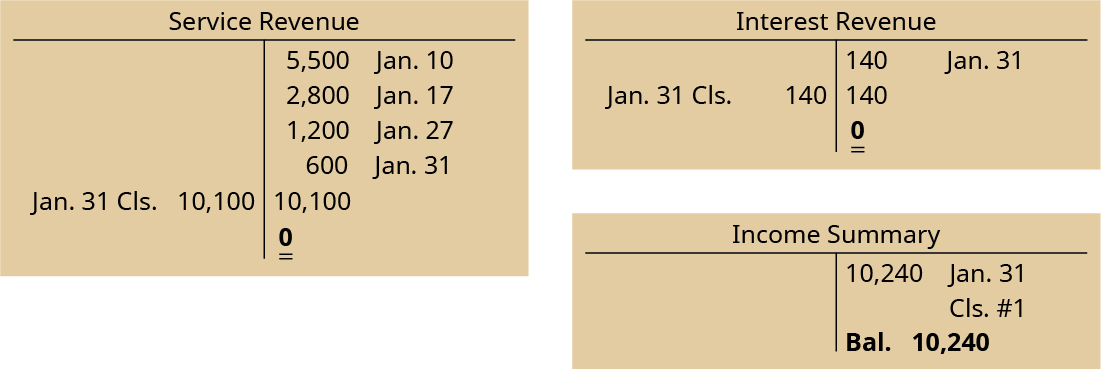

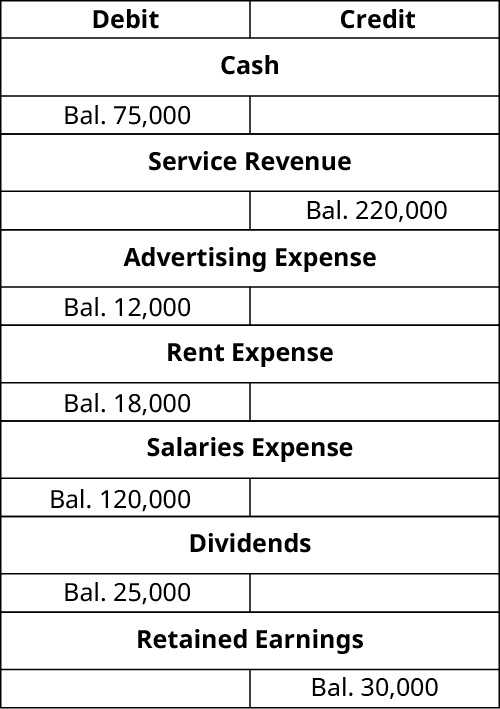

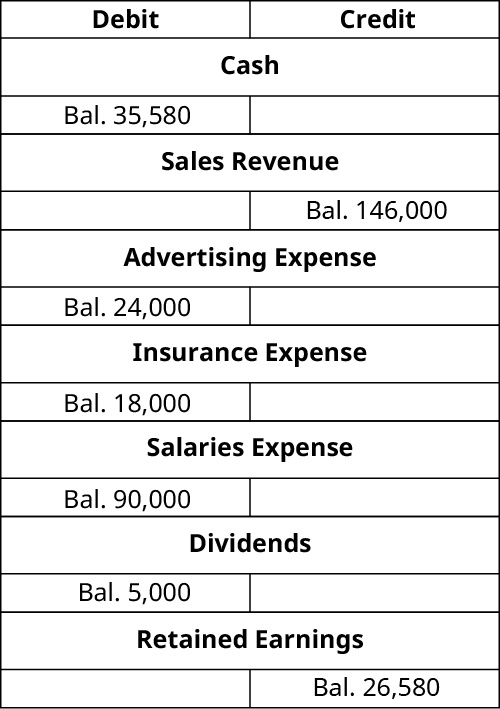

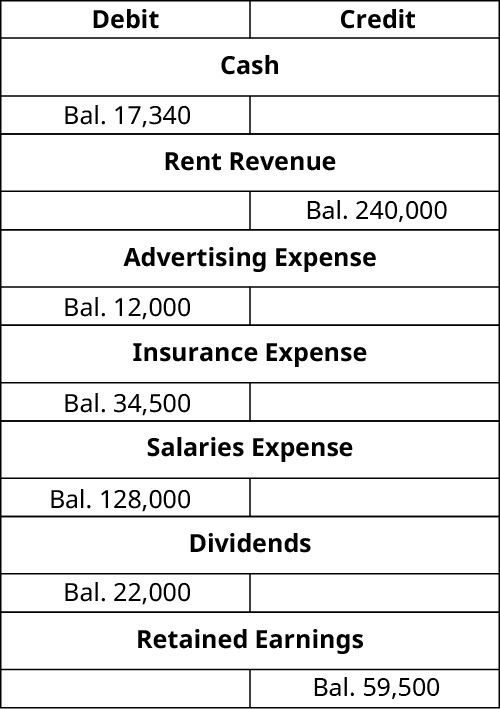

The starting time entry requires revenue accounts close to the Income Summary business relationship. To get a zero rest in a revenue account, the entry will show a debit to revenues and a credit to Income Summary. Press Plus has $140 of interest revenue and $10,100 of service revenue, each with a credit balance on the adjusted trial residual. The closing entry will debit both interest acquirement and service acquirement, and credit Income Summary.

The T-accounts after this closing entry would expect similar the post-obit.

Find that the balances in interest revenue and service acquirement are now zero and are ready to accumulate revenues in the side by side period. The Income Summary account has a credit residuum of $10,240 (the acquirement sum).

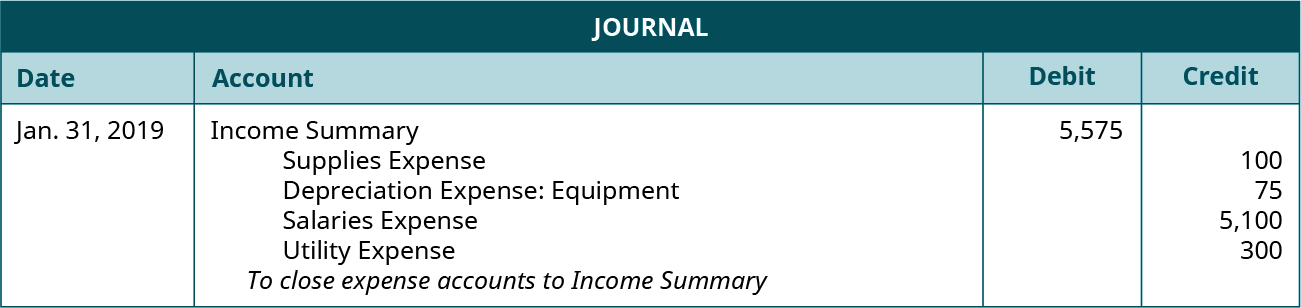

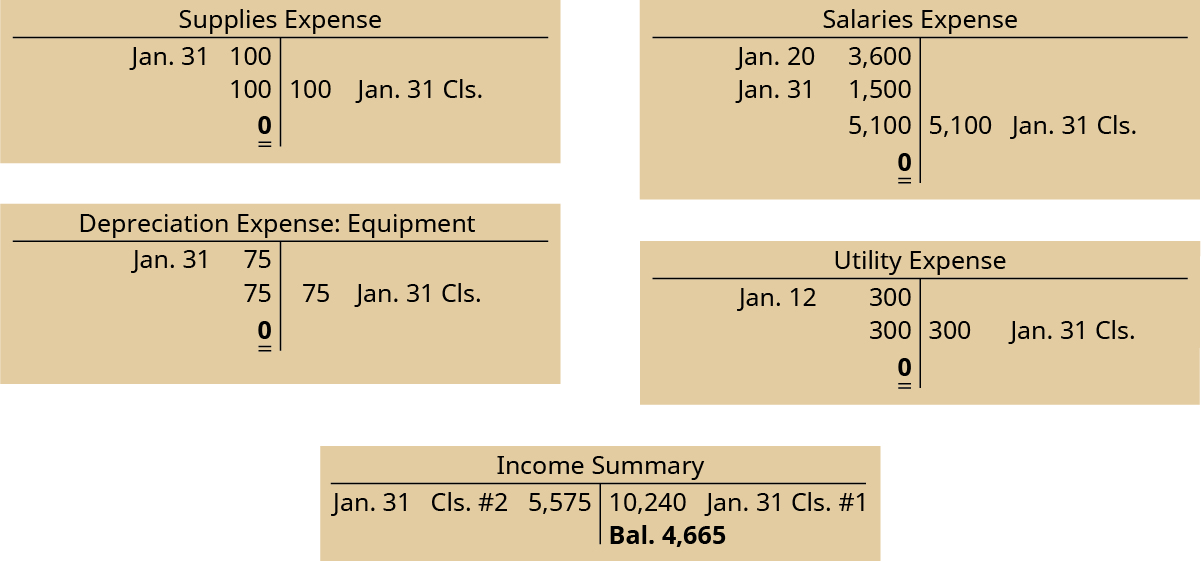

The second entry requires expense accounts close to the Income Summary business relationship. To get a zero remainder in an expense business relationship, the entry will show a credit to expenses and a debit to Income Summary. Printing Plus has $100 of supplies expense, $75 of depreciation expense–equipment, $v,100 of salaries expense, and $300 of utility expense, each with a debit residuum on the adjusted trial residue. The endmost entry will credit Supplies Expense, Depreciation Expense–Equipment, Salaries Expense, and Utility Expense, and debit Income Summary.

The T-accounts after this endmost entry would look like the following.

Notice that the balances in the expense accounts are now zip and are gear up to accumulate expenses in the adjacent menstruation. The Income Summary business relationship has a new credit balance of $4,665, which is the difference between revenues and expenses ((Effigy)). The balance in Income Summary is the same figure as what is reported on Printing Plus'south Income Statement.

Income Statement for Printing Plus. (attribution: Copyright Rice University, OpenStax, nether CC BY-NC-SA four.0 license)

Why are these 2 figures the aforementioned? The income argument summarizes your income, equally does income summary. If both summarize your income in the aforementioned catamenia, so they must be equal. If they do not lucifer, then you have an error.

The third entry requires Income Summary to close to the Retained Earnings business relationship. To become a zippo remainder in the Income Summary account, there are guidelines to consider.

- If the balance in Income Summary before closing is a credit balance, you will debit Income Summary and credit Retained Earnings in the closing entry. This state of affairs occurs when a company has a net income.

- If the balance in Income Summary before closing is a debit balance, you will credit Income Summary and debit Retained Earnings in the closing entry. This state of affairs occurs when a company has a cyberspace loss.

Remember that internet income will increase retained earnings, and a net loss will decrease retained earnings. The Retained Earnings account increases on the credit side and decreases on the debit side.

Press Plus has a $four,665 credit rest in its Income Summary account before closing, so it will debit Income Summary and credit Retained Earnings.

The T-accounts afterwards this endmost entry would look like the following.

Notice that the Income Summary business relationship is at present zilch and is set up for utilize in the side by side menses. The Retained Earnings account balance is currently a credit of $4,665.

The 4th entry requires Dividends to close to the Retained Earnings account. Remember from your past studies that dividends are not expenses, such every bit salaries paid to your employees or staff. Instead, declaring and paying dividends is a method utilized by corporations to render role of the profits generated by the company to the owners of the company—in this case, its shareholders.

If dividends were not declared, endmost entries would cease at this point. If dividends are declared, to become a zilch residual in the Dividends account, the entry will show a credit to Dividends and a debit to Retained Earnings. As you will learn in Corporation Accounting, there are iii components to the declaration and payment of dividends. The kickoff part is the date of annunciation, which creates the obligation or liability to pay the dividend. The second part is the date of record that determines who receives the dividends, and the third part is the date of payment, which is the engagement that payments are made. Printing Plus has $100 of dividends with a debit balance on the adjusted trial rest. The closing entry will credit Dividends and debit Retained Earnings.

The T-accounts after this endmost entry would look like the following.

Why was income summary not used in the dividends closing entry? Dividends are non an income statement account. Only income statement accounts help us summarize income, then just income statement accounts should go into income summary.

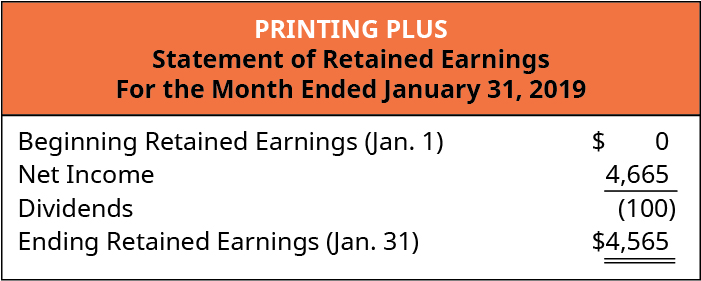

Remember, dividends are a contra stockholders' equity account. It is contra to retained earnings. If we pay out dividends, it means retained earnings decreases. Retained earnings decreases on the debit side. The remaining residue in Retained Earnings is $4,565 ((Figure)). This is the aforementioned figure plant on the argument of retained earnings.

Statement of Retained Earnings for Printing Plus. (attribution: Copyright Rice University, OpenStax, under CC BY-NC-SA 4.0 license)

The argument of retained earnings shows the period-ending retained earnings after the closing entries accept been posted. When yous compare the retained earnings ledger (T-account) to the argument of retained earnings, the figures must match. It is important to understand retained earnings is non closed out, information technology is only updated. Retained Earnings is the only account that appears in the closing entries that does not shut. Yous should recollect from your previous fabric that retained earnings are the earnings retained past the company over time—non cash flow just earnings. Now that we have closed the temporary accounts, let'southward review what the post-closing ledger (T-accounts) looks like for Press Plus.

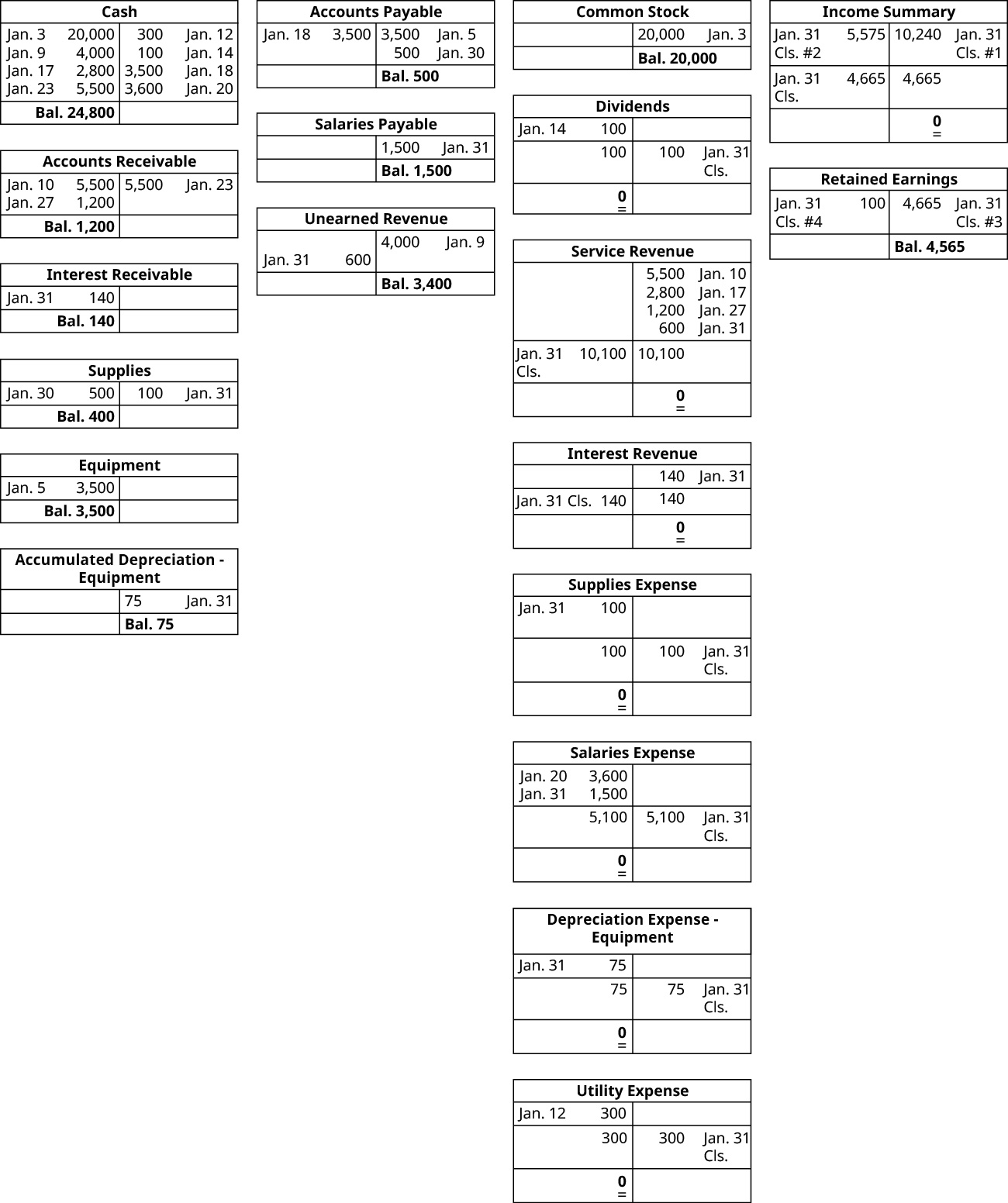

T-Account Summary

The T-account summary for Press Plus afterward endmost entries are journalized is presented in (Figure).

T-Account Summary. (attribution: Copyright Rice University, OpenStax, under CC BY-NC-SA 4.0 license)

Observe that revenues, expenses, dividends, and income summary all have zero balances. Retained earnings maintains a $4,565 credit rest. The post-closing T-accounts volition be transferred to the mail-closing trial balance, which is pace 9 in the accounting cycle.

Closing Entries

A company has revenue of $48,000 and total expenses of $52,000. What would the tertiary closing entry be? Why?

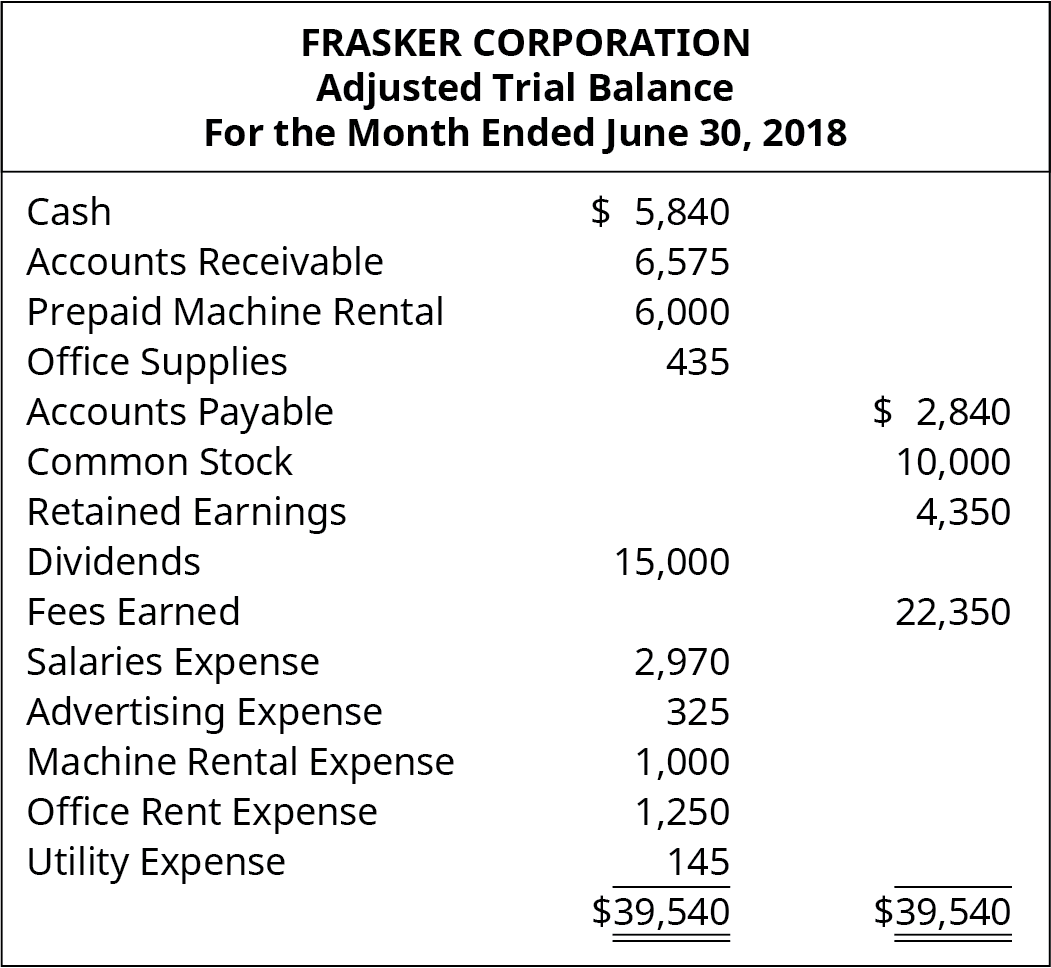

Frasker Corp. Closing Entries

Prepare the closing entries for Frasker Corp. using the adjusted trial balance provided.

Solution

Key Concepts and Summary

- Closing entries: Closing entries prepare a company for the side by side menstruum and zilch out balance in temporary accounts.

- Purpose of closing entries: Closing entries are necessary because they help a company review income aggregating during a menstruation, and verify data figures found on the adjusted trial rest.

- Permanent accounts: Permanent accounts do non close and are accounts that transfer balances to the next period. They include balance sheet accounts, such equally assets, liabilities, and stockholder's disinterestedness

- Temporary accounts: Temporary accounts are airtight at the end of each bookkeeping period and include income statement, dividends, and income summary accounts.

- Income Summary: The Income Summary business relationship is an intermediary between revenues and expenses, and the Retained Earnings account. Information technology stores all the endmost information for revenues and expenses, resulting in a "summary" of income or loss for the menses.

- Recording closing entries: In that location are 4 closing entries; closing revenues to income summary, closing expenses to income summary, closing income summary to retained earnings, and close dividends to retained earnings.

- Posting closing entries: Once all closing entries are complete, the information is transferred to the general ledger T-accounts. Balances in temporary accounts volition bear witness a zero balance.

Multiple Choice

(Figure)Which of the following accounts is considered a temporary or nominal business relationship?

- Fees Earned Revenue

- Prepaid Advertising

- Unearned Service Revenue

- Prepaid Insurance

(Figure)Which of the following accounts is considered a permanent or existent account?

- Interest Revenue

- Prepaid Insurance

- Insurance Expense

- Supplies Expense

(Figure)If a journal entry includes a debit or credit to the Greenbacks account, it is most likely which of the following?

- a closing entry

- an adjusting entry

- an ordinary transaction entry

- outside of the bookkeeping bike

(Figure)If a periodical entry includes a debit or credit to the Retained Earnings account, information technology is about likely which of the post-obit?

- a endmost entry

- an adjusting entry

- an ordinary transaction entry

- outside of the accounting bicycle

(Figure)Which of these accounts would be nowadays in the closing entries?

- Dividends

- Accounts Receivable

- Unearned Service Revenue

- Sales Tax Payable

(Figure)Which of these accounts would not be nowadays in the closing entries?

- Utilities Expense

- Fees Earned Revenue

- Insurance Expense

- Dividends Payable

(Figure)Which of these accounts is never closed?

- Dividends

- Retained Earnings

- Service Fee Acquirement

- Income Summary

(Figure)Which of these accounts is never closed?

- Prepaid Rent

- Income Summary

- Rent Acquirement

- Rent Expense

(Figure)Which account would be credited when closing the account for fees earned for the year?

- Accounts Receivable

- Fees Earned Revenue

- Unearned Fee Acquirement

- Income Summary

(Figure)Which account would exist credited when closing the account for rent expense for the yr?

- Prepaid Rent

- Hire Expense

- Rent Revenue

- Unearned Rent Revenue

Questions

(Figure)Explain what is meant by the term real accounts (also known as permanent accounts).

Real/permanent accounts are those that comport over from i menstruum to the next, with a continuing balance in the account. Examples are asset accounts, liability accounts, and disinterestedness accounts. In contrast, revenue accounts, expense accounts, and dividend accounts are not real/permanent accounts.

(Figure)Explain what is meant by the term nominal accounts (likewise known as temporary accounts).

(Figure)What is the purpose of the closing entries?

Closing entries are used to transfer the contents of the temporary accounts into the permanent account, Retained Earnings, which resets the temporary balances to zero, enabling tracking of revenues, expenses, and dividends in the side by side period.

(Figure)What would happen if the company failed to make closing entries at the terminate of the twelvemonth?

(Figure)Which of these business relationship types (Assets, Liabilities, Equity, Acquirement, Expense, Dividend) are credited in the closing entries? Why?

Expense accounts and dividend accounts are credited during closing. This is because endmost requires that the business relationship balances be cleared, to ready for the next accounting period.

(Effigy)Which of these business relationship types (Assets, Liabilities, Equity, Revenue, Expense, Dividend) are debited in the endmost entries? Why?

(Figure)The account called Income Summary is oft used in the endmost entries. Explain this account'south purpose and how it is used.

Income Summary is a super-temporary account that is only used for closing. The revenue accounts are closed by a debit to each account and a corresponding credit to Income Summary. Then the expense accounts are closed past a credit to each account and a corresponding debit to Income Summary. Finally, the balance in Income Summary is cleared past an entry that transfers its residual to Retained Earnings. Thus, it is used in three journal entries, every bit part of the endmost procedure, and has no other purpose in the bookkeeping records.

(Figure)What are the 4 entries required for endmost, assuming that the Income Summary business relationship is used?

(Figure)Later the starting time two closing entries are made, Income Summary has a credit balance of $125,500. What does this indicate about the company's net income or loss?

The fact that Income Summary has a credit rest (of any size) later the outset two endmost entries are made indicates that the company made a cyberspace profit for the period. In this example, a credit of $125,500 reflects the fact that the company earned net income of $125,500 for the catamenia.

(Figure)After the offset two closing entries are fabricated, Income Summary has a debit balance of $22,750. What does this indicate about the visitor'south internet income or loss?

Exercise Prepare A

(Figure)Identify whether each of the post-obit accounts is nominal/temporary or real/permanent.

- Accounts Receivable

- Fees Earned Revenue

- Utility Expense

- Prepaid Rent

(Effigy)For each of the post-obit accounts, identify whether it is nominal/temporary or real/permanent, and whether it is reported on the Balance Sail or the Income Statement.

- Interest Expense

- Buildings

- Interest Payable

- Unearned Rent Revenue

(Figure)For each of the following accounts, identify whether information technology would be airtight at year-terminate (yes or no) and on which financial statement the account would be reported (Balance Sheet, Income Statement, or Retained Earnings Argument).

- Accounts Payable

- Accounts Receivable

- Greenbacks

- Dividends

- Fees Earned Revenue

- Insurance Expense

- Prepaid Insurance

- Supplies

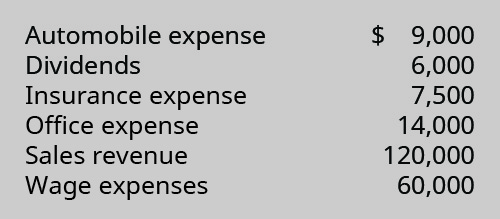

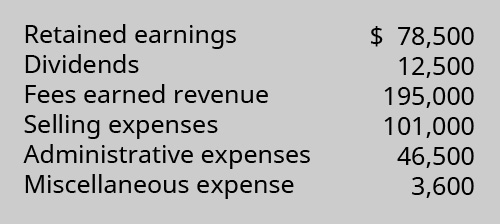

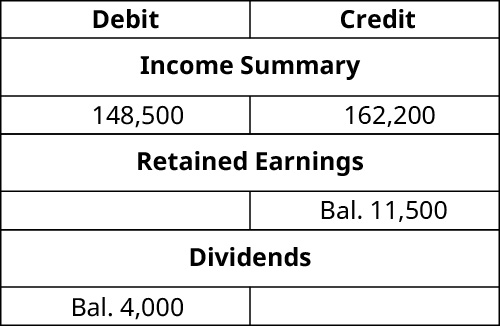

(Figure)The post-obit accounts and normal balances existed at yr-cease. Make the four journal entries required to close the books:

(Effigy)The following accounts and normal balances existed at year-stop. Make the iv journal entries required to close the books:

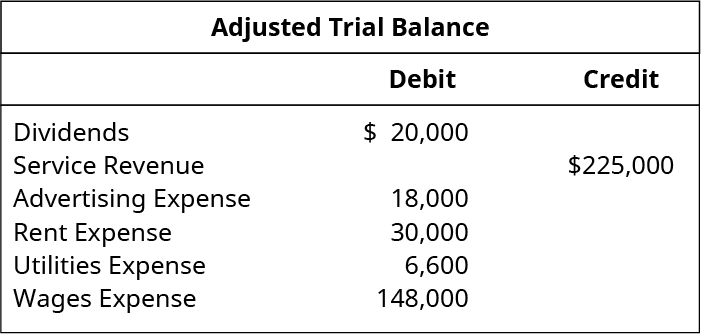

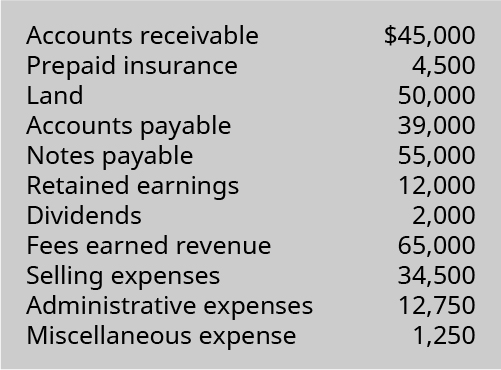

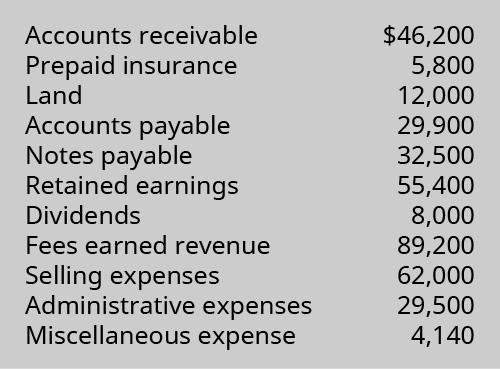

(Figure)Use the following excerpts from the yr-end Adjusted Trial Residual to prepare the 4 periodical entries required to close the books:

(Figure)Utilize the post-obit T-accounts to prepare the iv journal entries required to close the books:

(Figure)Employ the following T-accounts to prepare the iv journal entries required to close the books:

Exercise Set B

(Figure)Identify whether each of the post-obit accounts are nominal/temporary or real/permanent.

- Hire Expense

- Unearned Service Fee Revenue

- Involvement Revenue

- Accounts Payable

(Effigy)For each of the following accounts, place whether it is nominal/temporary or real/permanent, and whether information technology is reported on the Balance Canvass or the Income Statement.

- Salaries Payable

- Sales Revenue

- Salaries Expense

- Prepaid Insurance

(Figure)For each of the following accounts, identify whether it would exist closed at twelvemonth-end (yes or no) and on which financial statement the account would be reported (Balance Canvas, Income Argument, or Retained Earnings Statement).

- Retained Earnings

- Prepaid Rent

- Rent Expense

- Rent Revenue

- Salaries Expense

- Salaries Payable

- Supplies Expense

- Unearned Rent Revenue

(Figure)The following accounts and normal balances existed at year-end. Brand the four journal entries required to close the books:

(Figure)The post-obit accounts and normal balances existed at year-stop. Make the four journal entries required to close the books:

(Effigy)Use the following excerpts from the year-end Adjusted Trial Balance to fix the iv periodical entries required to close the books:

(Figure)Employ the following T-accounts to fix the four journal entries required to close the books:

(Figure)Use the following T-accounts to gear up the four journal entries required to close the books:

Trouble Set A

(Figure)Place whether each of the following accounts would be considered a permanent account (yes/no) and which financial argument it would exist reported on (Balance Sheet, Income Statement, or Retained Earnings Argument).

- Accumulated Depreciation

- Buildings

- Depreciation Expense

- Equipment

- Fees Earned Revenue

- Insurance Expense

- Prepaid Insurance

- Supplies Expense

- Dividends

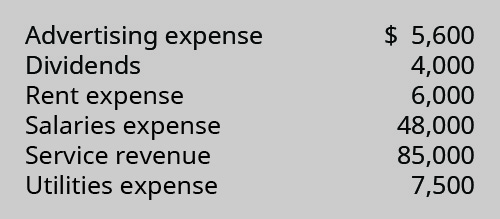

(Effigy)The following selected accounts and normal balances existed at year-end. Make the 4 journal entries required to close the books:

(Figure)The following selected accounts and normal balances existed at yr-terminate. Notice that expenses exceed revenue in this period. Make the iv journal entries required to close the books:

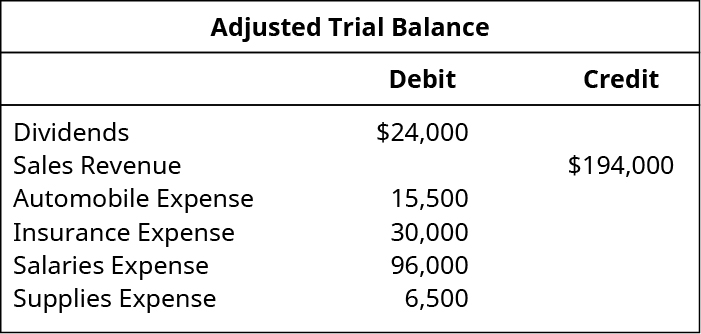

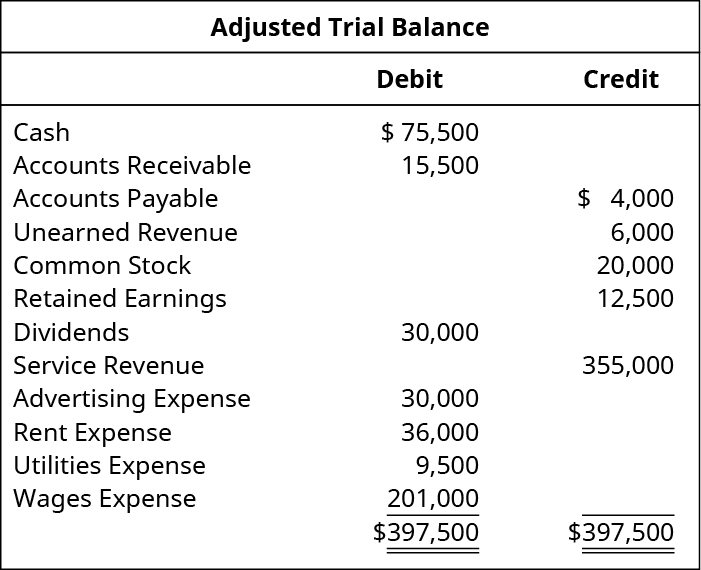

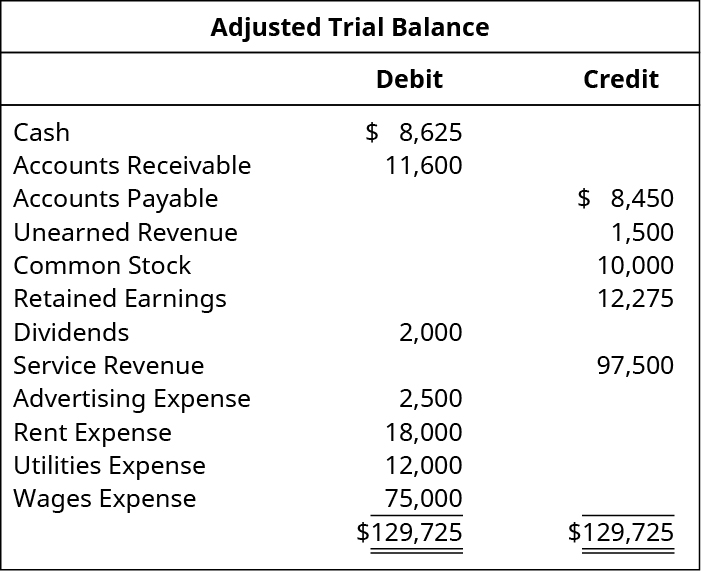

(Figure)Utilize the following Adjusted Trial Balance to prepare the iv journal entries required to close the books:

(Figure)Use the following Adapted Trial Residual to prepare the four journal entries required to close the books:

(Effigy)Utilize the following T-accounts to prepare the 4 journal entries required to close the books:

(Figure)Assume that the first 2 closing entries have been made and posted. Use the T-accounts provided as follows to:

- complete the closing entries

- determine the catastrophe balance in the Retained Earnings account

Problem Set B

(Figure)Identify whether each of the post-obit accounts would be considered a permanent account (yes/no) and which fiscal statement it would be reported on (Balance Sheet, Income Argument, or Retained Earnings Argument).

- Mutual Stock

- Dividends

- Dividends Payable

- Equipment

- Income Tax Expense

- Income Taxation Payable

- Service Revenue

- Unearned Service Acquirement

- Net Income

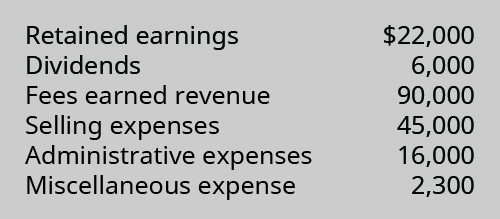

(Figure)The following selected accounts and normal balances existed at year-end. Brand the iv journal entries required to close the books:

(Figure)The following selected accounts and normal balances existed at year-end. Detect that expenses exceed acquirement in this period. Brand the iv journal entries required to close the books:

(Effigy)Use the following Adapted Trial Rest to prepare the four journal entries required to shut the books:

(Figure)Use the following Adjusted Trial Balance to prepare the four journal entries required to close the books:

(Figure)Use the post-obit T-accounts to prepare the four journal entries required to close the books:

(Figure)Presume that the first two closing entries take been made and posted. Use the T-accounts provided below to:

- complete the closing entries

- determine the ending residuum in the Retained Earnings business relationship

Thought Provokers

(Figure)Presume you are the controller of a large corporation, and the principal executive officeholder (CEO) has requested that yous refrain from posting endmost entries at 20X1 year-terminate, with the intention of combining the ii years' profits in year 20X2, in an effort to make that year's profits appear stronger.

Write a memo to the CEO, to offer your response to the request to skip the closing entries for twelvemonth 20X1.

(Figure)Search the Securities and Exchange Commission website (https://www.sec.gov/edgar/searchedgar/companysearch.html) and locate the latest Course 10-1000 for a company you would similar to clarify. Submit a curt memo:

- Land the name and ticker symbol of the company you take chosen.

- Review the company'south stop-of-period Residue Canvass, Income Statement, and Statement of Retained Earnings.

- Use the data in these financial statements to answer these questions:

- If the company had used the income summary account for its closing entries, how much would the company have credited the Income Summary account in the first closing entry?

- How much would the company have debited the Income Summary account in the 2nd closing entry?

Provide the web link to the company'due south Course x-Thousand, to allow accurate verification of your answers.

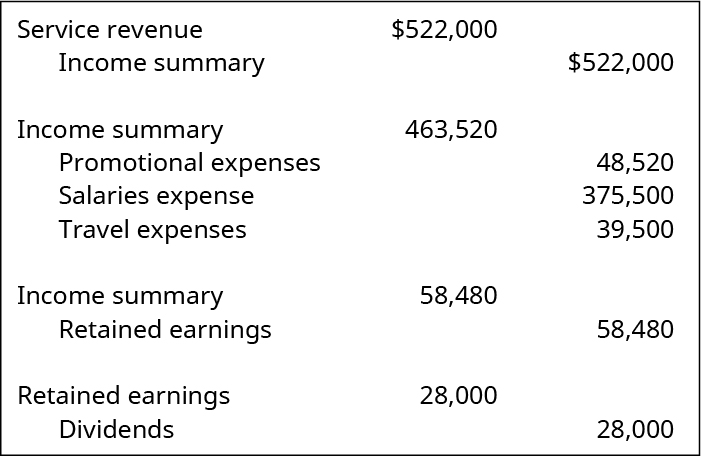

(Figure)Assume you are a senior accountant and accept been assigned the responsibleness for making the entries to close the books for the year. You take prepared the following four entries and presented them to your dominate, the principal financial officer of the visitor, along with the company CEO, in the weekly staff meeting:

As the CEO was reviewing your work, he asked the question, "What do these entries mean? Can we larn anything about the company from reviewing them?"

Provide an explanation to requite to the CEO near what the entries reveal virtually the company's operations this year.

Glossary

- endmost

- returning the account to a zero balance

- closing entry

- prepares a company for the next accounting catamenia by clearing any outstanding balances in certain accounts that should non transfer over to the side by side catamenia

- income summary

- intermediary between revenues and expenses, and the Retained Earnings account, storing all the closing information for revenues and expenses, resulting in a "summary" of income or loss for the catamenia

- permanent (existent) account

- account that transfers balances to the next period, and includes remainder canvass accounts, such equally assets, liabilities, and stockholder's disinterestedness

- post-closing trial balance

- trial residue that is prepared after all the closing entries take been recorded

- temporary (nominal) account

- account that is airtight at the terminate of each accounting menstruation, and includes income statement, dividends, and income summary accounts

Source: https://opentextbc.ca/principlesofaccountingv1openstax/chapter/describe-and-prepare-closing-entries-for-a-business/

Posted by: harrellgare1973.blogspot.com

0 Response to "Which Of The Following Accounts Does Get Closed? A. Service Revenue"

Post a Comment